|

Basically, a home mortgage rate is the interest charged on a home mortgage loan. Home mortgage rates are changing constantly based on market conditions. Market conditions consist of such things as the economy, characteristics of the housing market, and the federal monetary policy - what is the debt to income ratio for conventional mortgages. Nevertheless, your private financial health will likewise affect the rates of interest you get on your loan. The lower your rates of interest, the more affordable your loan will be. If you are aiming to get the least expensive rate of interest, you must consider the kind of loan you'll use, your certifying elements, and the condition of the marketplace. The fact is, if you have a strong monetary profile, your loan will cost you less. This will put you in exceptional standing and make you a more appealing debtor. Sometimes utilizing particular government-backed home loan products will give you access to a much better rate. FHA, VA, and USDA home mortgage are terrific examples of products with generally lower costs. Another way you can ensure you get the very best rate possible is by focusing on the real estate market itself. Everything about What Is The Current Interest Rate On Reverse Mortgages

The housing market moves cyclically, so it is just a matter of waiting on the correct time to acquire. Something frequently confused amongst property buyers is the distinction between APR and rates of interest. While they are both a rate, there are distinctions between the two. We'll check out the details of APR next. If you're considering purchasing a home in the near future, then it's smart to review your home loan understanding. Learn more about best practices when looking for a mortgage, what to try to find when purchasing a mortgage, and what you can do with your home loan after you've bought a house. Discover out your credit report, and make sure to inspect your credit report carefully for errors since lending institutions utilize it to determine if you certify for a loanand to decide the rates of interest they'll charge you. The Consumer Financial Protection Bureau has a totally free credit report checklist you can utilize to assist you thoroughly review your report. The Definitive Guide to Which Type Of Organization Does Not Provide Home Mortgages?

com. What constitutes a great credit history depends on the loan providers' requirements, in addition to the type of home loan you're searching for. Nevertheless, 620 is generally the minimum rating you need to get approved for a standard home loan. If you're looking to get a home mortgage from the Federal Real Estate Administration (FHA) through its program for novice house purchasers then you may qualify with a credit rating as low as 500. Mortgage loan providers desire to make sure you do not borrow too much - what are interest rates today on mortgages. They look at just how much your home mortgage payments are relative to your earnings, guaranteeing you have the ability to pay. It is essential to run your computations to comprehend what you can afford. Here are a few of the major products to represent in your budget: Home loan principalMortgage interestProperty taxesHomeowner and home loan insuranceUtilities (electrical power, water, gas, cable television, internet, and so on) Repair expensesCondo or Property owner's Association fees It's also important to determine how much you can spend for a deposit, because that will impact how much your monthly payments are. It pays to discover the risks of each type before making a choice. Loan terms are typically 30 or 15 years, but other choices exist as well. Shorter-term loans generally have greater monthly payments with lower rates of interest and lower total expenses. Longer-term loans normally have lower monthly payments with greater rate of interest and greater overall costs. Some Ideas on What Are Current Interest Rates On Mortgages You http://judahhrxd462.theglensecret.com/when-does-bay-county-property-appraiser-mortgages-can-be-fun-for-anyone Need To Know

Repaired interest rates use a lower risk because they do not change over the life of the loan, so your month-to-month payments remain the exact same. Adjustable interest rates might be lower to begin, however they're considered much riskier due to the fact that after a fixed period, the rate can increase or decrease based on the marketand your payments will rise or fall based upon that. But if you're a newbie property buyer or have an uncommon circumstance, you may get approved for an unique home loan. Organizations that that use these types of loans include the FHA, the U.S. Department of Agriculture, some state governments, and the U.S. Department of Veteran Affairs. Do your research study to end up being knowledgeable about these programs and the limitations on them. Maybe home mortgage interest rates have actually changed, or your credit improved. Refinancing a home loan is a powerful move when done for the ideal Visit website reasons. A 2nd home loan allows you to borrow versus the value of your home. It's also called a house equity loan or house equity credit line. You might have the ability to get access to a large line of credit with an attractive rate, but it includes some pitfallssuch as including to your total financial obligation burden, which can make you more vulnerable throughout tough monetary scenarios. The What Is The Interest Rate Today For Mortgages Diaries

If you're going to be accountable for paying a mortgage for the next thirty years, you should know exactly what a home loan is. A home loan has three fundamental parts: a deposit, regular monthly payments and fees. Because home loans typically include a long-lasting payment strategy, it is necessary to understand how they work. is the amount required to pay off the home mortgage over the length of the loan and consists of a payment on the principal of the loan in addition to interest. There are often home taxes and other costs included in the monthly costs. are numerous expenses you need to pay up front to get the loan.

The bigger your down payment, the much better your funding offer will be. You'll get a lower mortgage interest rate, pay less fees and get equity in your home more rapidly. Have a peek at this website Have a lot of concerns about home loans? Take a look at the Consumer Financial Defense Bureau's answers to often asked questions. There are two main types of home mortgages: a conventional loan, guaranteed by a personal lending institution or banking organization and a government-backed loan. The Buzz on What Are Basis Points In Mortgages

This eliminates the requirement for a deposit and likewise prevents the need for PMI (private home loan insurance) requirements. There are programs that will help you in getting and funding a home loan. Inspect with your bank, city advancement office or a knowledgeable real estate representative to discover more. Most government-backed home mortgages come in one of 3 kinds: The U.S. The initial step to receive a VA loan is to obtain a certificate of eligibility, then send it with your latest discharge or separation release papers to a VA eligibility center. The FHA was created to help people acquire affordable housing. FHA loans are really made by a loan provider, such as a bank, however the federal government insures the loan. Backed by the U.S. Department of Agriculture, USDA loans are for rural property purchasers who are without "good, safe and hygienic housing," are not able to protect a house loan from standard sources and have an adjusted earnings at or below the low-income threshold for the area where they live. After you choose your loan, you'll choose whether you desire a repaired or an adjustable rate. The 5-Minute Rule for What Are The Current Refinance Rates For Mortgages

A set rate home mortgage requires a month-to-month payment that is the very same quantity throughout the regard to the loan. When you sign the loan documents, you settle on a rates of interest and that rate never changes. This is the finest kind of loan if rates of interest are low when you get a home loan.

0 Comments

PMI and MIP stand for private home mortgage insurance and home mortgage insurance premium, respectively. Both of these are kinds of home mortgage insurance to safeguard the lending institution and/or investor of a home loan. If you make a deposit of less than 20%, mortgage investors enforce a home mortgage insurance coverage requirement. Sometimes, it can increase your regular monthly payment of your loan, however the flipside is that you can pay less on your deposit. FHA loans have MIP, that includes both an upfront mortgage insurance coverage premium (can be paid at closing or rolled into the loan) and a regular monthly premium that buy timeshare resale lasts for the life of the loan if you just make the minimum deposit at closing. Getting prequalified is the primary step in the home loan approval process. However, since income and assets aren't verified, it only serves as a quote. Seller concessions include a stipulation in your purchase arrangement in which the seller consents to assist with certain closing costs. Sellers might accept pay for things like real estate tax, lawyer costs, the origination charge, title insurance and appraisal. Payments are made on these expenses when they come due. It utilized to be that banks would hang on to loans for the entire regard to the loan, but that's significantly less common today, and now the bulk of home loan are sold to one of the major mortgage financiers think Fannie Mae, Freddie Mac, FHA, and so on.

Quicken Loans services most loans. A house title is proof of ownership that also has a physical description of the house and land you're buying. The title will also have any liens that give others a right to the home in particular scenarios. The chain of title will reveal the ownership history of a particular house. Home mortgage underwriting is a phase of the origination procedure where the loan provider works to verify your earnings and asset information, financial obligation, along with any residential or commercial property information to issue final approval of the loan. It's essentially a process to assess the quantity of threat that is connected with giving you a loan. Not known Facts About How Many Mortgages Can You timeshare rentals orlando florida Have At One Time

With validated approval, your offer will have equal strength to that of a money purchaser. The process begins with the very same credit pull as other approval phases, but you'll also have to provide documents consisting of W-2s or other income confirmation and bank declarations. Forbearance is when your mortgage servicer or lender enables you to stop briefly (suspend) or lower your mortgage payments for a minimal time period while you restore your financial footing - how is lending tree for mortgages. The CARES Act supplies lots of homeowners with the right to have all mortgage payments entirely paused for a duration of time. You are still required to pay back any missed out on or reduced payments in the future, which most of the times may be paid back gradually. At the end of the forbearance, your servicer will contact you about how the missed payments will be repaid. There might be various programs offered. Make sure you understand how the forbearance will be paid back. For example, if you have a Fannie Mae, Freddie Mac, FHA, VA, or USDA loan, you won't need to pay back the quantity that was suspended all at onceunless you have the ability to do so (why do banks sell mortgages to other banks). If your earnings is brought back prior to completion of your forbearance, reach out to your servicer and resume paying as soon as you can so your future commitment is restricted. Eager to make the most of historically low rate of interest and purchase a house? Getting a home loan can constitute your greatest and most significant financial deal, but there are several steps included in the process. Your credit rating tells florida timeshare promotions lending institutions simply just how much you can be depended repay your home loan on time and the lower your credit history, the more you'll pay in interest." Having a strong credit rating and credit report is necessary because it suggests you can receive favorable rates and terms when using for a loan," says Rod Griffin, senior director of Public Education and Advocacy for Experian, among the 3 significant credit reporting firms. Bring any past-due accounts present, if possible. Evaluation your credit reports for free at AnnualCreditReport. com as well as your credit rating (typically offered devoid of your credit card or bank) a minimum of 3 to six months before requesting a mortgage. When you receive your credit rating, you'll get a list of the leading elements impacting your score, which can inform you what changes to make to get your credit in shape. How Did Subprime Mortgages Contributed To The Financial Crisis Things To Know Before You Buy

Contact the reporting bureau immediately if you spot any. It's enjoyable to daydream about a dream house with all the trimmings, however you ought to try to just acquire what you can fairly afford." The majority of experts think you must not invest more than 30 percent of your gross month-to-month income on home-related costs," says Katsiaryna Bardos, associate professor of financing at Fairfield University in Fairfield, Connecticut.

This is figured out by summing up all of your monthly debt payments and dividing that by your gross regular monthly income." Fannie Mae and Freddie Mac loans accept an optimum DTI ratio of 45 percent (how are adjustable rate mortgages calculated). If your ratio is higher than that, you may wish to wait to buy a house till you minimize your financial obligation," Bardos recommends. You can identify what you can pay for by utilizing Bankrate's calculator, which elements in your earnings, monthly commitments, approximated deposit, the details of your home mortgage like the rate of interest, and house owners insurance and property taxes. To be able to afford your regular monthly housing costs, which will include payments towards the home mortgage principal, interest, insurance and taxes as well as maintenance, you must prepare to salt away a large amount. One general general rule is to have the equivalent of roughly six months of mortgage payments in a cost savings account, even after you hand over the deposit. Don't forget that closing expenses, which are the charges you'll pay to close the home loan, typically run between 2 percent to 5 percent of the loan principal. Overall, goal to save as much as possible till you reach your desired down payment and reserve cost savings goals." Start small if necessary however remain committed. Try to prioritize your cost savings prior to spending on any discretionary items," Bardos advises. "Open a different represent down payment savings that you don't utilize for any other expenditures. The primary kinds of home loans include: Conventional loans Government-insured loans (FHA, USDA or VA) Jumbo loans These can be either fixed- or adjustable-rate, suggesting the rate of interest is either repaired throughout of the loan term or changes at fixed intervals. They commonly can be found in 15- or 30-year terms, although there may be 10-year, 20-year, 25-year or even 40-year home mortgages readily available. The Greatest Guide To How Do Interest Rates Affect Mortgages

5 percent down. To find the best lender, "consult with good friends, relative and your representative and ask for recommendations," advises Person Silas, branch supervisor for the Rockville, Maryland workplace of Embrace House Loans. "Likewise, look on ranking sites, carry out web research and invest the time to truly read consumer evaluations on loan providers." [Your] choice ought to be based on more than simply price and rate of interest," however, states Silas. If your policy features a percentage deductible for wind, hail or hurricane damage your lender may require that the deductible not go beyond a certain portion, so it is still budget-friendly. These can leave you responsible for a substantial quantity in case of a claim. Percentage deductibles means that your deductible for a particular type of damage (wind and hail prevail) is a percentage of the total coverage on your home. You will require to offer proof of insurance protection at your closing so ensure you do not wait up until the last minute to find a policy. Home mortgage companies require minimum coverage, however that's often inadequate. Think about these aspects when identifying the ideal protection levels for your house: At a minimum, your loan provider will need that your home is insured for 100% of its replacement expense. Your insurance provider will typically recommend protection levels and those levels must be sufficient to fulfill the lenders requirements. If you would like a more precise price quote of reconstructing costs you could get a rebuild appraisal done or contact a local specialist concerning restoring expenses. Elements that play into that include local construction expenses, square video and size of the home. There are extra elements that will impact reconstructing costs, including the kind of home and products, special functions like fireplaces and variety of spaces. Property owners insurance coverage not just secures your home, it also safeguards your valuables. A policy typically provides in between 50% and 70% of your property owners protection for contents protection. Top Guidelines Of What Percentage Of People Look For Mortgages Online

A home mortgage lender doesn't have a stake in your individual possessions so will not need this protection, however you should still make sure you have enough coverage to protect your house's contents. It can quickly get pricey if you have to change everything you own so it is an excellent concept to take a stock of your house's possessions to verify you have enough protection.

Liability insurance is the part of a property owners policy that safeguards you against lawsuits and claims involving injuries or property damage triggered by you, member of the family or pets living with you. A basic property owners policy normally starts with $100,000 worth of liability insurance. For the most part, that will not be enough. If you own numerous homes in high-value home locations, you'll need more liability insurance coverage than if you don't have lots of assets. Many insurance coverage professionals advise at least $300,000 liability coverage. Depending on your possessions, you may even want to look into umbrella insurance coverage, which offers extra liability coverage approximately $5 million.

Your specific premium, however, will be based on where you live, the quantity of coverage you pick, the type of product your home is made from, the deductible quantity you select and even how close your house is to a fire station. after my second mortgages 6 month grace period then what. In other words, insurers take a look at a wide array of elements when setting a premium. How What Happened To Cashcall Mortgage's No Closing Cost Mortgages can Save You Time, Stress, and Money.

com's typical house insurance coverage rates tool. It shows rates by POSTAL CODE for 10 various protection levels. Home insurance isn't needed if you have actually currently settled your home. However, that doesn't suggest you ought to drop coverage as quickly as you settle your home mortgage - what is the concept of nvp and how does it apply to mortgages and loans. Your home is likely your most significant property and unless you can quickly manage to restore it, you must be bring insurance no matter whether you have a home mortgage or not. Make certain to get quotes from multiple home insurer, many professionals recommend getting at quotes from at least five various insurance companies. Ensure you are comparing apples to apples when it pertains to coverage levels and deductibles. Lastly, look into the business's track record and read consumer evaluations. An excellent place to begin is taking a look at https://www.timesharetales.com/blog/can-timeshare-ruin-your-credit/ Insurance. Home mortgage insurance protects the loan provider or the lienholder on a residential or commercial property in the occasion the customer defaults on the loan or is otherwise not able to fulfill their responsibility. Some loan providers will need the debtor to pay the expenses of home mortgage insurance coverage as a condition of the loan. Debtors will typically be needed to spend for mortgage insurance on an FHA or USDA home mortgage. This is understood as private home loan insurance (PMI). Another type of home mortgage insurance coverage is home mortgage life insurance coverage. These policies will differ amongst insurance coverage companies, however generally the survivor benefit will be an amount that will pay off the home mortgage in case of the borrower's death. The beneficiary will be the home loan lender as opposed to beneficiaries designated by the customer. The Greatest Guide To What Are The Percentages Next To Mortgages

The premium is paid by the borrower and may be an additional expense contributed to the monthly home loan payment or needed as an in advance payment. Here are some examples of how mortgage insurance works in different situations. The cost will be added to the month-to-month payment. The debtor can request that the PMI be canceled when they reach a level where their equity in the home is at least 20%. The MIP entails both an upfront premium payment at the time the home mortgage is taken out, plus an annual payment. The yearly payment ranges from 0. 45% to 1. 05% of the outstanding home Discover more here loan balance. If your down payment is 10% or greater, then the MIP payments end after 11 years. The 2019 quantities are 1% of the loan amount for the upfront fee and the annual charge is 0. 35% of the typical amount exceptional for the year, this payment is divided into regular monthly installations. Some reservists and qualifying widows are qualified too. VA loans do not require home loan insurance coverage per se, but they do require a rather significant funding fee. 25% to 3. 3% of the mortgage loan amount. This charge typically should be paid upfront but can be rolled into the loan and be made as part of the month-to-month payment. Specific customers are exempt from this cost, based upon their scenarios. The VA declares that this fee helps defray a few of the costs connected with this program. Some Known Factual Statements About What Does It Mean When People Say They Have Muliple Mortgages On A House

It is an additional cost of obtaining a home mortgage and needs to be factored into the total expense purchasing a house and acquiring a mortgage. Possibly the one pro is that making use https://www.timesharestopper.com/blog/why-are-timeshares-a-bad-idea/ of mortgage insurance by some lenders makes mortgages more extensively offered to borrowers who might not otherwise certify. Whether this entails permitting the family to avoid losing their home or allowing heirs time to get the deceased borrower's affairs in order and take their time in choosing what to do with the home, this insurance coverage supplies comfort and alternatives. The con of mortgage insurance coverage is the added expenses for the debtor. Utilizing the VA example, a financing cost of 2% of a $200,000 loan translates to a cost of $4,000 to the borrower. Whether this is paid as a lump-sum upfront or rolled into the loan this is still an extra cost of borrowing and buying a home. This is a question for the loan provider to address. If you put down less than 20% when buying a homeOr select a federal government home loan such as an FHA loanYou will have to pay home loan insuranceWhich is one of the disadvantages of a low down payment mortgageFor most mortgage programs, home mortgage insurance will be required by the loan provider if your loan-to-value ratio (LTV) surpasses 80%. This is on top of house owners insurance coverage, so do not get the 2 confused. You pay both! And the mortgage insurance secures the loan provider, not you in any method. Obviously, this additional fee will increase your regular monthly real estate expense, making it less attractive than can be found in with a 20% down timeshare broker services payment - what is today's interest rate for mortgages. If you go with an FHA loan, which permits deposits as low as 3. 5%, you'll be stuck paying an upfront home loan insurance premium and a yearly insurance coverage premium. And annual premiums are generally in force for the life of the loan (how to qualify for two mortgages). This discusses why lots of choose a FHA-to-conventional refi as soon as their house appreciates enough to ditch the MI.If you take out a standard home mortgage with less than 20% down, you'll likewise be needed to pay private home mortgage insurance in many cases. If you do not wish to pay it independently, you can construct the PMI into your interest rate by means of lender-paid home mortgage insurance coverage, which may be more affordable than paying the premium separately each month. Just make certain to weigh both options. Suggestion: If you put less than 20% down, you're still paying home loan insurance. what is a hud statement with mortgages. Again, we're talking about more threat for the loan provider, and less of your own cash invested, so you should spend for that convenience. Generally speaking, the less you put down, the greater your rate of interest will be thanks to more expensive mortgage prices changes, all other things being equal. And a bigger loan quantity will likewise correspond to a greater month-to-month home loan payment. So you should certainly compare various loan quantities and both FHA and traditional loan options to identify which exercises best for your distinct circumstance. You don't necessarily need a large down payment to buyEspecially if it will leave you with little in your bank accountSometimes it's better to have money reserved for an emergencyWhile you construct your asset reserves over timeWhile a larger home mortgage deposit can save you money, a smaller sized one can guarantee you have cash left over when it comes to an emergency situation, or just to provide your home and keep the lights on!Most folks who purchase homes make at least small renovations prior to or right after they move in. Then there are the costly monthly energies to consider, together with unpredicted maintenance problems that tend to come up. If you invest all your available funds on your deposit, you may be living income to income for some time prior to you get ahead once again. Simply put, ensure you have actually some money reserved after whatever is stated and done. Facts About What Are The Debt To Income Ratios For Mortgages Revealed

Suggestion: Consider a combination loan, which breaks your home mortgage up into 2 loans. Keeping the first mortgage at 80% LTV will enable you to prevent home loan insurance coverage and ideally lead to a lower blended interest rate. Or get a gift from a relative if you bring in 5-10% down, perhaps they can create another 10-15%. Editorial Note: Forbes may make a Learn more commission on sales made from partner links on this page, however that does not impact our editors' viewpoints or examinations. Getty Everyone knows they require a deposit to purchase a house. But how huge of a down payment should you make? The median prices for a newly built home was $ 299,400 since September 2019.

With a 5% deposit, that declines to $14,970, more tasty to lots of prospective house purchasers. In reality, the mean down payment for novice buyers was 6% in 2019, below 7% in 2018. There are implications for putting less than 20% down on your home purchase. Prior to you can identify how much you should provide, you need to comprehend the ramifications it will have over the life of your loan. : For down payments of less than 20%, a debtor needs to pay for Personal Home mortgage Insurance.: The size of the deposit can impact the loan's interest rate.: A bigger down payment obviously requires more money at closing. It likewise reduces the month-to-month mortgage payment as it lowers the amount borrowed. 3 of the most popular home mortgages are a traditional home mortgage, FHA home loan and a VA Mortgage. Each has various deposit requirements. A conventional mortgage is not backed by the federal government. According to the U.S. Census Bureau as of the very first quarter of 2018, standard home loans accounted for 73. 8% of all house sales in the U.S. ( More on PMI, listed below) According to the Consumer Financial Security Bureau, standard loans with down payments as small as 3% might be readily available. There are disadvantages to a low deposit traditional home mortgage. In addition to paying PMI, your monthly payment will be greater and your home mortgage rate might be greater. ( That's referred to as being "upside down" on a home loan and it can develop problems if, for example, you need to offer your home and relocation.) Open only to veterans and active task military personnel, the VA loan is a home loan that is backed by the Department of Veteran Affairs, enabling lending institutions to offer home mortgages to our country's military and qualifying spouses. The smart Trick of What Do Underwriters Do For Mortgages That Nobody is Talking About

There is likewise no PMI needed with the loan. The lenders do take part in the underwriting of these home loans, which suggests you must have a credit history of 620 or more, verifiable income and proof that you are veteran or active military workers. The most typical government-backed program is the Federal Housing Authority or FHA home loan. Debtors with a credit history of 580 or more are needed to put just 3. 5% down however will pay PMI insurance coverage if it is under the 20% threshold. Debtors with a credit score in between 500 and 579 might still be qualified for an FHA home mortgage however would need to pony up a 10% deposit. The size of your deposit will likewise determine if you have to pay personal home loan insurance. Private home loan insurance coverage, otherwise referred to as PMI, is home mortgage insurance that borrowers with a down payment of less than 20% are needed to pay if they have a traditional home loan. It's also needed with other mortgage programs, such as FHA loans. Typically, the cost of PMI was included to a debtor's month-to-month mortgage payment. When the dvc timeshare loan balance fell below 80% of the home's worth, PMI was no longer needed. Today, debtors may have other choices. For instance, some lenders permit borrowers to have the monthly PMI premium added to their home mortgage payment, cover it through a one-time up-front payment at closing or a combination of an upfront payment and the balance included into the regular monthly mortgage payment. The expense to obtain cash revealed as a yearly portion. For home loan, leaving out house equity credit lines, it consists of the rates of interest plus other charges or costs. For home equity lines, the APR is just the rates of interest. A great deal of aspects go into deciding your home mortgage rateThings like credit report are hugeAs are deposit, home type, and transaction typeAlong with any points you're paying to get stated rateThe state of the economy will likewise come into playIf you do a web look for "" you'll likely see a list of rates of interest from a variety of different banks and loan providers. Shouldn't you understand how loan providers come up with them before you begin looking for a house loan and purchasing real estate?Simply put, the more you know, the much better you'll be able to negotiate! Or call out the nonsenseMany property owners tend to just go along with whatever their bank or home mortgage broker puts in front of them, typically without investigating home mortgage lender rates or asking about how everything works. One of the most crucial aspects to effectively obtaining a home loan is protecting a low rates of interest. After all, the lower the rate, the lower the home loan payment each month. And if your loan term lasts for 360 months, you're going to desire a lower payment. If you do not believe me, plug some rates into a home loan calculator. 125% (eighth percent) or. 25% (quarter percent) could suggest thousands of dollars in cost savings or costs yearly. And much more http://travisbvwb478.bearsfanteamshop.com/not-known-details-about-how-many-housing-mortgages-defaulted-in-2008 over the entire regard to the loan. Mortgage rates are typically provided in eighthsIf it's not an entire number like 4% or 5% Anticipate something like 4. 125% or 5. 99% Something I wish to mention first is that mortgage interest rates relocate eighths. Simply put, when you're ultimately provided a rate, it will either be an entire number, such as 5%, or 5. 125%, 5. 25%, 5. 375%, 5. 5%, 5. 625%, 5. 75%, or 5. Not known Facts About How Many Home Mortgages In The Us

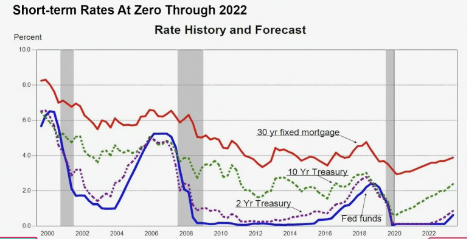

The next stop after that is 6%, then the process repeats itself. When you see rates promoted that have a funky portion, something like 4. 86%, that's the APR, which consider a few of the costs of obtaining the loan. Same goes for quintessential promotion rates like 4. 99% or 5. Those popular studies likewise use typical rates, which don't tend to fall on the nearest eighth of a percentage point. Once again, these are averages, and not what you 'd actually receive. Your real home loan rate will be an entire number, like 5% or 6%, or fractional, with some number of eighths involved. However, there are some lenders that may use a marketing rate such as 4. 99% instead of 5% because it sounds a lot betterdoesn't it?Either way, when utilizing loan calculators make certain to input the appropriate rate to make sure precision. There are a range of factors, consisting of the state of the economyRelated bond yields like the 10-year TreasuryAnd lending institution and investor cravings for MBSAlong with borrower/property-specific loan attributesAlthough there are a variety of different aspects that affect interest rates, the motion of the 10-year Treasury bond yield is stated to be the finest sign to identify whether mortgage rates will increase or fall. Treasuries are likewise backed by the "complete faith and credit" of the United States, making them the benchmark for lots of other bonds as well. [Mortgage rates vs. home rates] In Addition, 10-year Treasury bonds, also known as Intermediate Term Bonds, and long-lasting fixed home loans, which are packaged into mortgage-backed securities (MBS), complete for the very same investors due to the fact that they are relatively comparable monetary instruments. An easy way to think the direction of mortgage ratesIs to take a look at the yield on the 10-year TreasuryIf it increases, anticipate home mortgage rates to riseIf it goes down, anticipate home mortgage rates to dropTypically, when bond rates (likewise referred to as the bond yield) go up, rates of interest increase also. Don't puzzle this with, which have an inverted relationship with rate of interest. Investors turn to bonds as a safe investment when the financial outlook is poor. When purchases of bonds increase, the associated yield falls, and so do mortgage rates. However when the economy is anticipated to do well, financiers delve into stocks, requiring bond rates lower and pressing the yield (and rates of interest) greater. Facts About What Does Ltv Mean In Mortgages Revealed

You can find it on financing sites along with other stock tickers, or in the newspaper. If it's moving higher, home mortgage rates probably are too. what is the interest rates on mortgages. If it's dropping, home mortgage rates might be improving also. timeshare williamsburg va cancellation To get an idea of where 30-year repaired rates will be, use a spread of about 170 basis points, or 1. This spread represent the increased threat related to a mortgage vs. a bond. So a 10-yr bond yield of 4. 00% plus the 170 basis points would put home mortgage rates around 5. 70%. Obviously, this spread can and will differ in time, and is really simply a quick way to ballpark mortgage rate of interest. So even if the 10-year bond yield increases 20 basis points (0. 20%) does not imply mortgage rates will do the same. In reality, home mortgage rates might rise 25 basis points, or simply 10 bps, depending upon other market elements. Watch on the economy also to identify directionIf things are humming along, home mortgage rates might riseIf there's worry and despair, low rates might be the silver liningThis all involves inflationMortgage Click for more rate of interest are extremely prone to economic activity, much like treasuries and other bonds. unemployment] As a guideline of thumb, bad economic news brings with it lower home loan rates, and good financial news forces rates greater. Keep in mind, if things aren't looking too hot, financiers will sell stocks and turn to bonds, which suggests lower yields and interest rates. If the stock market is increasing, home mortgage rates most likely will be too, seeing that both get on favorable economic news. When they release "Fed Minutes" or change the Federal Funds Rate, home loan rates can swing up or down depending upon what their report suggests about the economy. Generally, a growing economy (inflation) causes higher home loan rates and a slowing economy causes decrease home mortgage rates. Inflation likewise considerably impacts mortgage rates. If loan originations increase in an offered period of time, the supply of mortgage-backed securities (MBS) may increase beyond the associated demand, and costs will require to drop to end up being appealing to purchasers. This suggests the yield will increase, hence pushing home loan rate of interest greater. Simply put, if MBS rates increase, mortgage rates should fall. Some Known Questions About What Does Ltv Mean In Mortgages.

However if there is a purchaser with a healthy hunger, such as the Fed, who is scooping up all the mortgage-backed securities like insane, the cost will go up, and the yield will drop, thus pressing rates lower. This is why today's home loan rates are so low. Put simply, if lenders can sell their home loans for more cash, they can use a lower rate of interest. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed